Realizing Engine Value

Sales to BX JV puts a "!" on their worth

January 25, 2024

Willis Lease Finance Corporation (WLFC): It trades on the NASDAQ, but management already treats it as their own private company. Management tried to take it private three times. Liquidation value is within $5 of $45. It cost 69% of stated tangible book value or closer to 65% of current TBV. They earned over $2 per share in three of the last four quarters and can maintain that run rate. Their majority shareholder offered to take private at $50 per share last year but the independent committee rejected the lowball bid. There could be a Russia recovery of over $20 million this year.

WLFC’s primary business is leasing spare aircraft engines to airlines. They own around 350 engines. Tangible book value per share is about $67, but there is a lot more value if you fair value the balance sheet assets. The engines are carried at the lower of appraised value or depreciated value. Most are carried at depreciated value. However, an engine typically rises in value in the first three to five years. With the current inflationary environment the values are even worth more today than historically. Backing into the market value based on the values disclosed in their asset backed securities, there is at least $60 per share of value not reflected in book value related to the fair value of the engines.

WLFC is positioned well for the current rate environment. They have legacy asset-backed security issuance that has an all in cost of around 4%. The did another this past month that is about 8% cost, which will take overall funding up some.

The management owns about 57% of the company and has tried to take it private three times, but hasn’t been successful. The most recent offer was earlier this year for $50 per share but the independent committee of board members was not willing to accept the inadequate price. The negative is management compensation is way too high and unnecessary expenses (use of corporate aircraft, yacht, etc.) are a drag on earnings, but shares are inexpensive enough to still make this a great investment. There are multiple routes to getting capital returned: they could do a modified Dutch tender (they have done two before), a capital distribution/special dividend, a sale of the company, or another attempt to take it private.

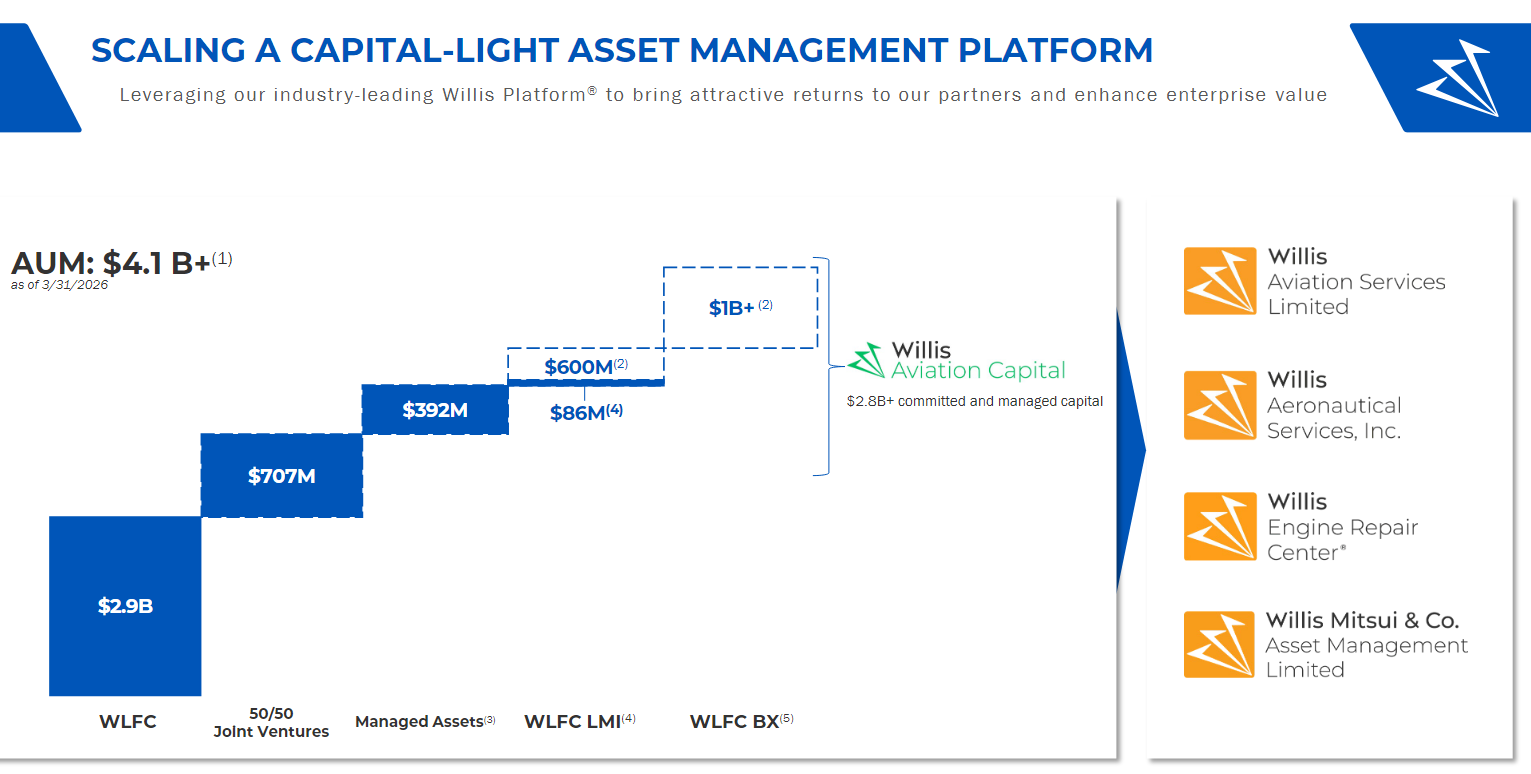

May 5, 2026

WLFC is countercyclical. They do better when airlines are struggling as now (keeping later stage airplanes flying instead of just retiring them and buying new OEM planes).

Their big news is that they started selling assets from WLFC’s engine portfolio to the Blackstone (BX) JV last month.

This quarter looked solid. Next quarter will look gaudy because of the asset sales. The market likes this quarter so far but will like next more.

This idea was for a 10% allocation to WLFC at $50 or lower. So far, so good but I’d reiterate the original caveat:

Willis’ management don’t treat minority holders as if we’re owed more than a nominal premium for our shares in a management led buyout. They will have to shift their view in order to do a fair deal.

For better and for worse, insiders run this as if it were already private. They are egregiously overcompensated. They act like they want outside holders to just go away. We can oblige for a fair price.