2 Kinds of M&A

What still works.

Spiking volatility and interest rates are not the friends of M&A. Many deals require financing that is unavailable today. Boards want to have more market stability before they buy or sell. Deal volume has collapsed. What is there to do? What still works? I see two deal types that still work in such times.

Busted Biotechs

Biotechs are capital intensive. They need to hire expensive talent to work on expensive development programs long before they make any money. When they succeed, they’re generally triumphant deal targets. When they fail, they can be disasters for equity holders.

Their carcasses can be valuable if you can buy them at a deep enough discount to their cash. The key is to understand how fast they burn that cash and how aligned the board and management are with their shareholders. The best outcome is to get sold for a premium to cash to a buyer that puts any value on their remaining science projects. The worst outcome is to overpay for another try in a reverse merger. In between is simply liquidating and distributing available cash before it is gone.

For example, Keros recently announced a strategic review. Anyone who owns any shares should contact their board and management to advocate for a sale or liquidation instead of a reverse merger or some effort to keep it going. In a deal environment when few deals can get done, this type of deal can. It is perfect for shareholders: it can hand us a profit, liquidity, and simplicity as long as insiders don’t screw us.

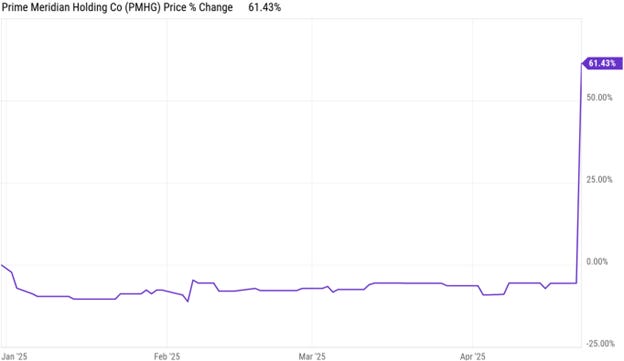

Credit Union Deals

Credit unions are tax advantaged financial institutions with little oversight on their deals. In theory their depositors are owners, but none are able to effectively advocate for depositor value. Credit unions can buy banks and are utterly insensitive to the prices that they pay. For one of several recent examples, MidFlorida Credit Union is buying Prime Meridian Bank (PMHG) for $58.50 per share in cash. Shares last traded for $49.56 per share, offering a ~18% IRR if the deal closes this time next year. Using a 10% discount rate, the deal consideration has around a net present value of ~$53 per share, quite a premium for shares that last traded ~$29.

Caveat

Both the busted biotechs and the credit union deal targets can be small and illiquid; they both work better as baskets.

Conclusion

I like both KROS and PMHG. I love the next ones.

TL; DR

If you own KROS or PMHG, they’re worth hanging onto them in their respective announced processes (KROS’ strategic review and PMHG’s definitive but not yet completed sale). If you’re interested in more potential deal targets, I hope to have more to share here.